After nearly three decades of deflation, Japan has experienced a sustained rise in prices since 2022, marking a potential turning point for its economy. This reflation phase was initially triggered by external factors such as surging commodity prices and a weaker yen but has now evolved into a domestic dynamic driven by wage growth and services price increases.

Japan is at a historic crossroads. For this reflation to translate into sustainable price growth, wage increases must continue, and companies need to convert profits into productive investments. Without this, the country risks falling back into the deflation trap.

Junyu Tan, Coface economist, North Asia

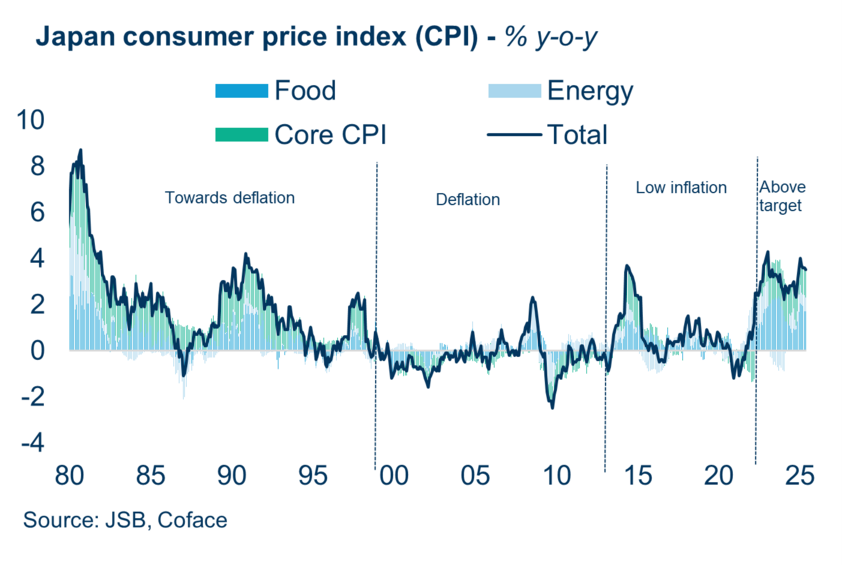

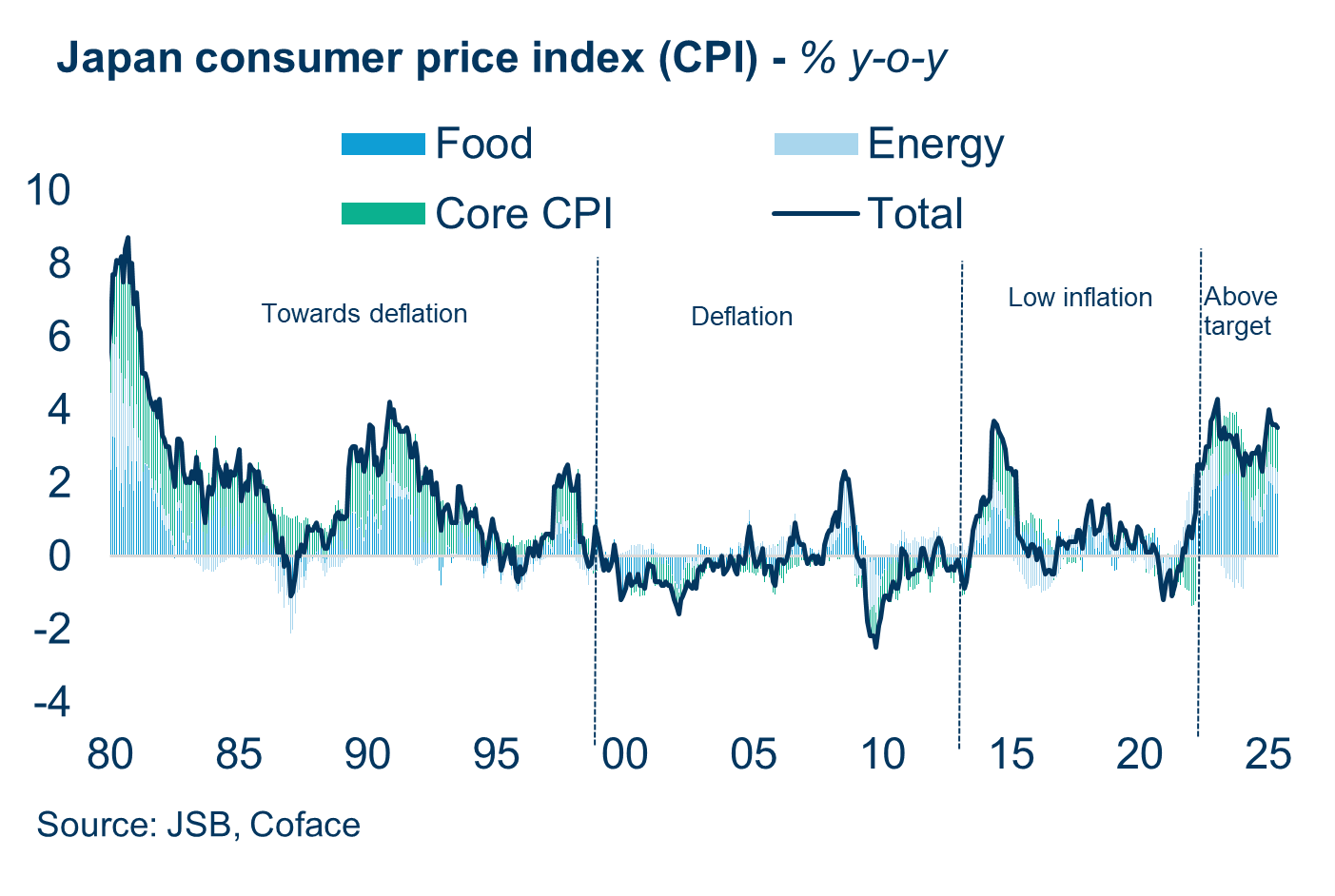

From structural deflation to sustained inflation

Since the collapse of the asset price bubble in the early 1990s, Japan has experienced a period of disinflation followed by prolonged deflation. As land and asset prices plummeted, households and firms prioritized debt repayment over consumption and investment, contributing to what is often referred to as a “balance sheet recession.”

Over the past three decades, occasional inflationary episodes occurred, mostly driven by temporary shocks such as oil price spikes or consumption tax hikes, without lasting pull from domestic demand. This has changed since 2022, when inflation consistently exceeded the Bank of Japan’s 2% target, fuelled initially by rising import costs and yen depreciation.

What began as cost-push inflation has gradually evolved into a demand-driven phenomenon. Service companies, facing sustained margin pressure, accelerated price pass-through to consumers. Rising living expenses along with structural labour market tightness, in turn, empowered labor unions to negotiate significant wage increases for three consecutive years: 3.6% in 2023, 5.1% in 2024, and 5.3% in 2025, the highest in three decades. This wage growth represents a profound shift away from Japan’s historical focus on job security toward stronger compensation demands.

(data for the graph in .xls format)

Wages, productivity, and investment: keys to a sustainable cycle

The continuation of Japan’s reflationary cycle now hinges on the ability of companies to sustain wage increases through productivity-enhancing investment. After decades of cash hoarding and under-investment, Japanese companies have begun to significantly ramp up capital expenditures since 2022. Average annual investment growth reached 9.1% between 20221 and 2024, with a further 6.7% increase expected for the current fiscal year.

Investments are particularly strong in automation and labour-saving technologies, designed to address Japan’s chronic labor shortages. At the same time, research and development (R&D) spending is rising in fast-growing segments such as chips and green energy, spurred by government incentives and corporate governance reforms promoted by the Tokyo Stock Exchange.

Whether these investments will translate into real productivity gains remains an open question. But without them, labor shortages will continue to act as a bottleneck on corporate revenue growth, ultimately suppressing wage growth and undermining the reflationary cycle.

Winners and losers in a new economic landscape

The reflationary environment has already reshaped Japan’s corporate landscape, creating clear winners and losers. Large exporting companies have benefited from the weaker yen, which has boosted overseas earnings, particularly for automobile and electrical machinery firms. Profits in these sectors have more than doubled compared to pre-COVID levels, supported by strong global demand for hybrid vehicles and production reshoring. However, this momentum may be challenged by rising U.S. tariffs and improving yen strength.

Domestic sectors such as catering and transport are also thriving. Their profits have been boosted by rising domestic consumption and a surge in inbound tourism. For many service providers, a virtuous wage-price cycle has emerged, enabling them to raise prices without sacrificing demand, thereby offsetting higher labor costs

By contrast, small and medium-sized enterprises (SMEs), which employ around 70% of Japan’s workforce, face mounting challenges. Limited pricing power and tighter margins make it difficult for them to absorb rising labor costs. As a result, corporate bankruptcies among SMEs have been increasing since the second half of 2022, though the level remains well below the peaks seen during the Asian Financial Crisis and the Global Financial Crisis.

Over time, this “clean-up” may ultimately strengthen Japan’s corporate ecosystem by reallocating resources toward more productive firms.

(data for the graph in .xls format)

Download the full 2025 Focus on Japan now.

1 Japan’s fiscal year runs from April-1st to March-31st of the following year