The global economy weathered the trade turmoil of the first half of 2025, but the coming quarters will see a spreading of the longer-term effects. The October 2025 Coface Risk Review analyses global dynamics, placing its focus on the surge in social and political risk, and the strategic challenges facing the Gulf countries.

In this context, Coface has made 5 changes to country assessments (including 4 upgrades) and 16 changes to sector assessments (including 9 upgrades). Check them in the Business Risk Dashboard.

Key trends

- Coface global growth forecast: +2.6% in 2025, +2.4% in 2026

- +4%: increase in corporate insolvencies in advanced economies in the first half of 2025.

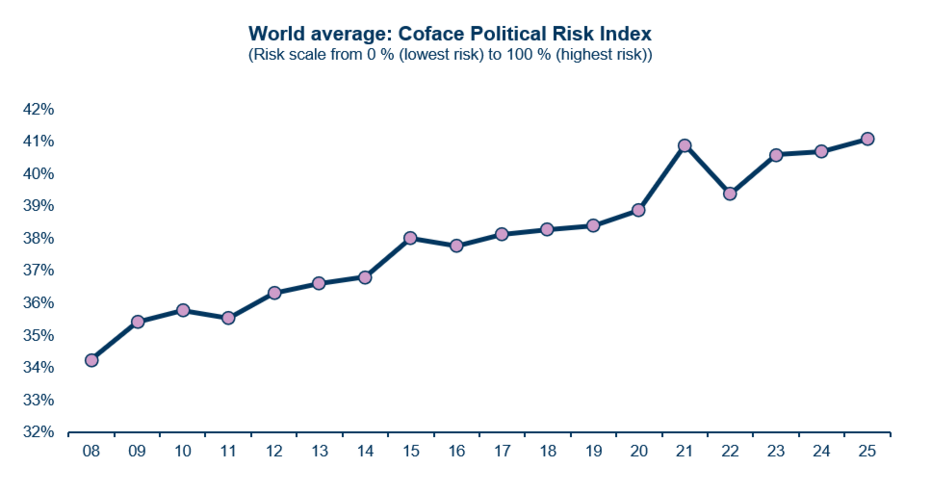

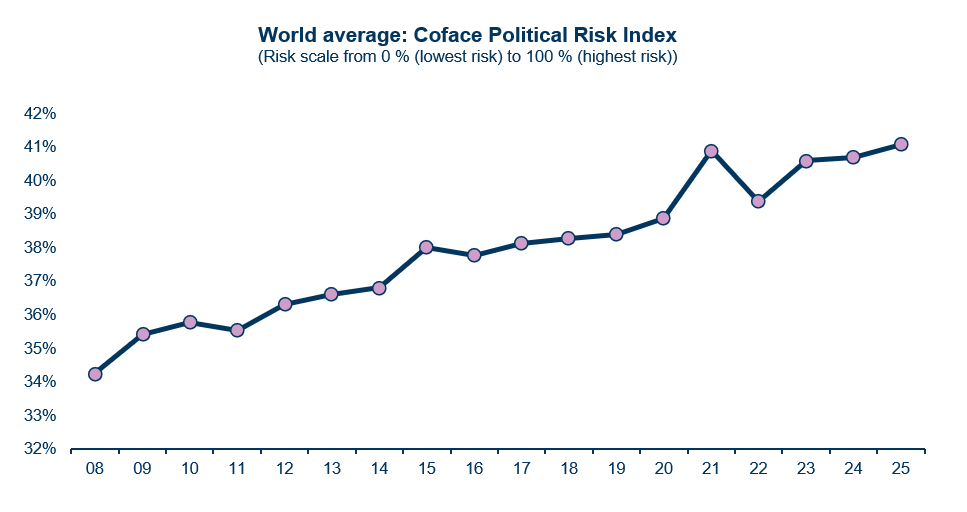

- A historic high on the Coface Political and Social Risk Index: 41.1% (+2.8 pp compared to the pre-pandemic average)

- 70% of the Gulf's GDP now comes from the non-oil sector (end of 2024).

The global economy absorbs the shock of new tariffs

After a summer marked by trade agreements and a gradual rise in US tariffs, the global economy is showing surprising resilience. The average US tariff rate now stands at around 18% (after peaking at 36% just after Liberation Day), well above the 2.5% observed under the Biden administration. Companies have been able to anticipate, reorient and absorb the shocks, and the US economy has also been supported by strong investment in artificial intelligence. However, the first negative signs for activity, employment and inflation are appearing in the US, heralding a gradual transfer of the harmful effects of customs measures to the macroeconomy.

Coface forecasts global growth of +2.6% in 2025 – revised upwards slightly – followed by +2.4% in 2026. The US is holding up better than expected for the time being, thanks to domestic demand, while China is expected to continue to slow and eurozone growth will remain sluggish, despite the (minor) rebound expected in Germany. Inflationary pressures continue to be low in the context of global slowdown and falling commodity prices (energy and food), but uncertainty prevails over the profile of US inflation, which is expected to be around 4% at the end of 2025 or the beginning of 2026. On the central bank front, the Fed resumed its rate-cutting cycle in September, while the ECB has probably finished its – barring a sharp deterioration in activity – after setting a deposit rate of 2%.

At the regional level, India has been posting remarkable growth (+7.6 % in the first half of the year), Poland is maintaining solid momentum (+3.4 %), while Africa’s outlook is improving (+4.1 % in 2025). However, the economic situation remains uncertain given the risks of geopolitical escalation and the effects of fiscal tightening in the countries where it has been introduced.

Rise in insolvencies: Europe and Asia on the front line

Business insolvencies have continued to rise in 2025. The overall index for advanced economies is up 4% compared to 2024, with marked increases in Europe (+11%) and Asia-Pacific (+12%), while North America remains stable. While lower interest rates and easier access to credit should provide some relief in 2026, the current trend underscores the fragility of businesses grappling with high costs and uncertain demand.

Political and social risk: instability has become the norm

The Coface social and political risk index has reached a historic high of 41.1%, surpassing the pandemic peak and establishing political risk as a key structural parameter of the global economy.

data for the graph in .xls format

Major conflicts persist, while domestic tensions are intensifying, particularly in Africa (Burkina Faso, Niger, etc.), Pakistan and Lebanon. The US has seen the sharpest rise in risk, which is related to growing institutional fragility and a rise in populism. In Europe, France is facing a major and unprecedented political crisis. The context is forcing companies to be increasingly vigilant and to continuously adapt their strategies.

Oil: the Gulf reinvents its power

The Gulf Cooperation Council (GCC) continues to be one of the most dynamic regions, driven by accelerated economic diversification: the non-oil sector will account for nearly 70 % of GDP by the end of 2024. GCC growth is expected to reach 3.8 % in 2025 and 4 % in 2026, supported by domestic demand and public initiatives (Vision 2030 in Saudi Arabia, among others).

The United Arab Emirates and Saudi Arabia have attracted record FDI1 flows (46 and 32 billion dollars respectively in 2024) and are strengthening their integration into global value chains. However, persistent dependence on hydrocarbons and a prolonged decline in oil prices would weaken budgets and could delay the completion of several major projects.

Our full forecasts and analysis in the Coface Risk Review (.pdf file)

1 Foreign Direct Investment