The 9th edition of the Coface survey on German companies' payment behaviour highlights a significant deterioration in payment terms, against a backdrop of political uncertainty and growing geopolitical tensions. Compared to the other countries surveyed by Coface, Germany however still stands out with some of the shortest payment terms and payment delays.

Payment terms: demand on the rise and at its highest level since 2016

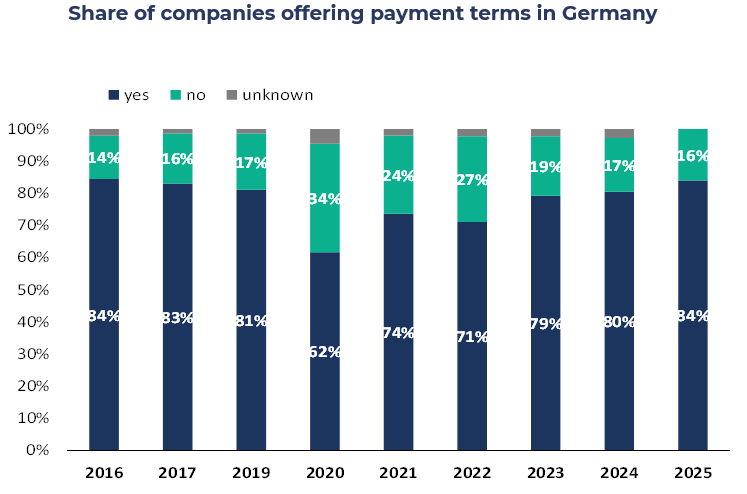

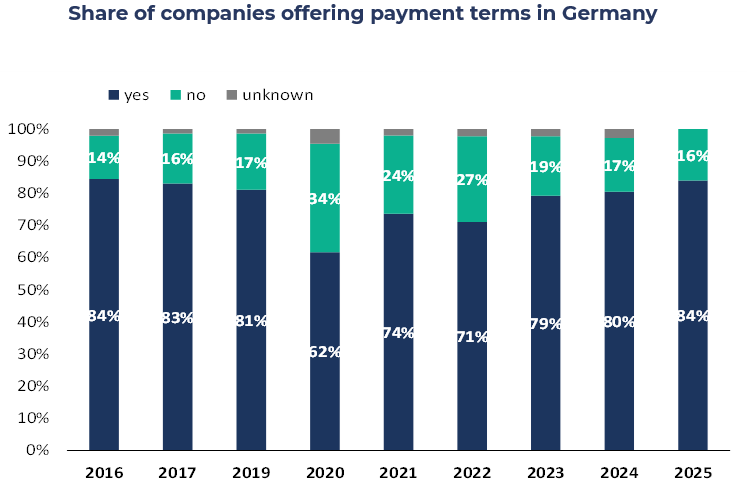

In 2025, 84% of German companies are granting payment terms, a record since 20162. At the same time, Germany's traditional preference for short payment terms has further strengthened: 92% of companies surveyed requested payment within 60 days, the same level as in 2016. Despite these changes, the average payment period remained almost unchanged at 32.5 days (compared to 32.1 in 2024).

data for the graph in xls format

Payment delays: on rise for the fourth consecutive year

81% of companies report new payment delays (+3%/2024), a figure close to the peak of 85% reached in 2019. The average length of payment delays increased by one day to 31.8 days. Although this marks a deterioration, the figure remains well below the pre-pandemic average (39.7 days).

Financial risk remains a concern, calling for caution in 2026

12% of companies reported long overdue payment (between six months and two years) exceeding 2% of their annual turnover. Although this figure is slightly down compared to 2024, it remains noticeably above the pre-pandemic average. The construction sector was the most affected, with 24% of companies reporting them. According to Coface's experience, 80% of these payment delays are never recovered, making them a significant commercial risk and a negative economic signal.

Economic outlook: fragile optimism amid ongoing uncertainty

After three years of economic stagnation, German companies are nevertheless seeing an improvement: while the overall sentiment remains negative for 2025 - the share of pessimists for 2025 are overweighing the share of optimists by 17 percentage points - , the outlook for 2026 is more encouraging with more optimists than pessimists (+16 points), buoyed by expected stimulus measures: investment in defence, infrastructure, climate transition and tax incentives for companies. All these measures induce some hope for Germany at the centre of the European economy, despite the political and economic challenges - both internal and external.

Germany remains a key market despite its challenges

Despite concerns about domestic demand and structural constraints, Germany together with the EU and EFTA3 countries remain the market considered most promising by the respondents. The United States however, lost its appeal and fell to the popularity levels last seen during the first term of Donald Trump. The back and forth in US- but also global trade policy is probably a main reason for that. Because of this, 23% of companies have already implemented ‘de-risking’ strategies (diversification of suppliers, payment security, relocation). According to the plans of our respondents, this figure is expected to reach 54% within the next three years, particularly in export-oriented sectors.

Although the outlook for 2026 has improved, we initially see a further deterioration in payment behaviour. This is also reflected in the insolvency figures, which are currently at a ten-year high.

Christiane von Berg, Regional Economist for Benelux, Germany, Austria and Switzerland at Coface.

Download the full study now

(.pdf 0,64 Mo)

[1] Survey conducted in May and June 2025 among 847 participating companies.

[1] Coface did not publish a payment survey in 2018.

[1] European Free Trade Association