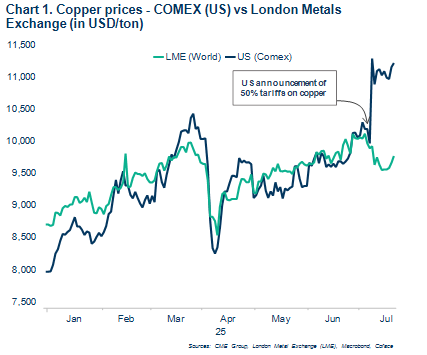

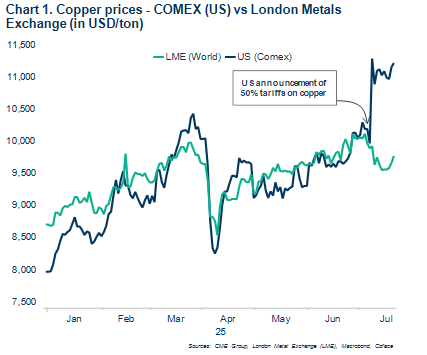

On July 8th, Donald Trump announced 50% tariffs on copper from August 1st, following a Section 232 investigation initiated by the White House in February. Nonetheless, their scope remains unclear, as there is currently no information on the nature of the taxed products — whether they apply to refined copper, derivative products, etc. Those tariffs are further fueling concerns within the US manufacturing sector, given that nearly half of the country’s copper demand is met through net imports.

US markets reacted sharply to rumours of tariff increases, triggering a record intraday spike on July 8th. COMEX copper futures surged by 13% on that day, reaching 11,290 USD per ton (chart 1). However, market dynamics remain fragmented: while prices on the London Metal Exchange (LME), the global benchmark, held relatively steady, domestic US prices rose significantly. The premium over LME prices fluctuated between 500 and 1,500 USD per ton in July, compared to an average of around 150 USD in 2024.

data for the graph in xls format

Further pressure on the American metals sector

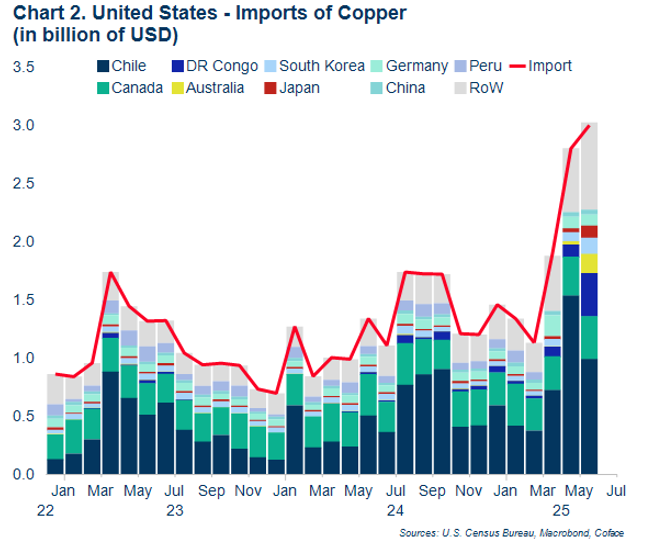

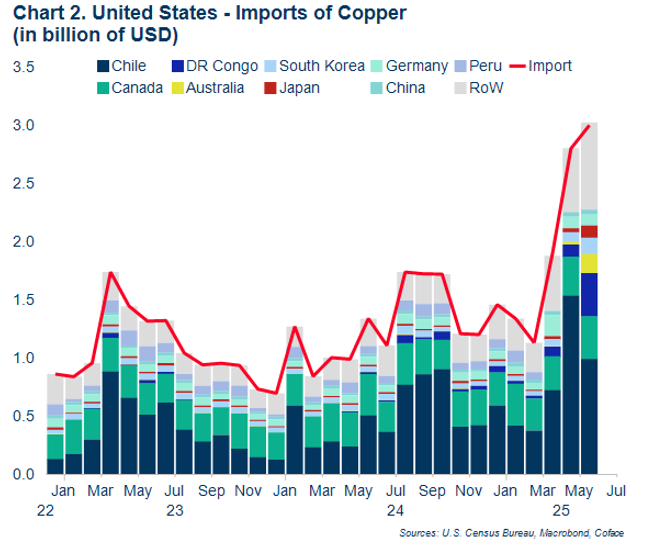

The US copper value chain relies on foreign supply, with net imports accounting for 45% of domestic consumption, with a total value of imports exceeding USD 17 billion in 2024. Last year, the US produced 3.5% of the world’s refined copper, while representing 6.3% of global consumption – pointing to a significant domestic supply gap. The sources of US foreign supply are also significantly concentrated in three countries with Chile, Canada, and Peru accounting for about 70% of its copper imports in 2024 (chart 2). These countries could be affected by a potential drop in demand resulting from rising prices on the US market. For now, prices appear to be stabilising as markets await further details on the scope of the tariffs. However, the most pessimistic forecasts predict US copper prices (COMEX) could reach 15,000 USD per ton, compared to approximately 11,000 USD per ton currently. US companies are likely to absorb the cost increase by compressing their margins, rather than passing higher copper prices on to consumers. Therefore, in the near term, these tariffs are expected to sap the financial health of US copper-related firms, such asbuilding materials and electrical wiring manufacturers, wind turbines producers, etc.

Nevertheless, we expect only a limited decline in US copper imports in the near-term, as domestic production capacity is insufficient to offset current US demand while global economic conditions should temper the surge in prices. Indeed, Chinese slowing demand and global over supply are expected to partially offset the impact of US trade barriers. Furthermore, according to Simon Lacoume, sector Analyst“we can expect that front-loaded purchases will ensure sufficient inventory levels through the end of the year in the US” (chart 2), reaching 240,000 tons in July, i.e. nearly 30% of projected consumption through year-end domestic consumption.

data for the graph in xls format

Chile on the Front Line of New US Tariff Measures

The access to the US market is crucial for Chile's copper sector. The US is its second-largest export market, accounting for 28.5% of total copper shipment, just behind China. Being the top export products, the country's copper flow to the US accounts for 5% of total Chilean shipment. Given this deep interdependence, rising tariffs would be a “lose-lose” situation. Codelco, the state-owned enterprise, is particularly vulnerable to the new trade barriers. Unlike its competitors, which operate across multiple regions and commodities, the state-owned firm is solely focused on domestic copper production. In 2024, Codelco accounted for a quarter of national copper production and contributed USD 1.5 billion to the state budget. A potential medium-term contraction in US demand, in response to the tariffs, would be particularly damaging for both the company and the Chilean state.